Humanoid Robots Market to Surge from USD 2.92 Bn to USD 29.57 Bn

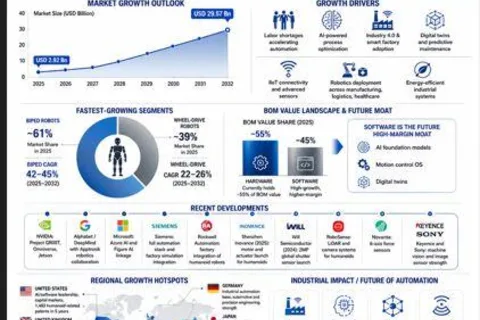

Humanoid Robots Market size was valued at USD 2.92 billion in 2025 and is expected to reach USD 29.57 billion by 2032, expanding at a CAGR of 39.2% during 2025-2032, according to Maximize Market Research. The market is entering a decisive growth cycle as labor shortages, AI-powered robotics, smart factory modernization, advanced sensors, predictive maintenance, digital twins, and next-generation process control converge to reshape industrial productivity. MMR positions humanoid robotics as a strategic infrastructure market, driven by the need to automate physical and cognitive work across manufacturing, logistics, healthcare, retail, public services, and personal assistance applications. The humanoid robotics industry is shifting from experimental deployment to early commercial scaling. Manufacturers are no longer evaluating humanoid robots as isolated automation assets; they are assessing them as flexible, AI-enabled labor platforms that can operate within human-built environments. The result is a new phase of industrial transformation in which humanoid robots support production lines, warehouse workflows, quality inspection, maintenance operations, material movement, and repetitive factory tasks while integrating with IIoT systems, machine vision, edge AI, and cloud-based robotics platforms. Industry 4.0 Adoption Moves Humanoid Robots from Lab Prototypes to Smart Factories The strongest market momentum is emerging from Industry 4.0 adoption. Enterprises are digitizing manufacturing systems, connecting shop floors through IIoT, deploying predictive maintenance tools, and investing in real-time operational intelligence. Humanoid robots fit directly into this transition because they can use human-like mobility, computer vision, natural language interfaces, and adaptive learning to work in facilities already designed for people. MMR highlights the market's long-run labor addressable opportunity at more than USD 60 trillion, reflecting the scale of tasks that could eventually be augmented or automated by humanoid systems. The report also notes that generative AI, labor scarcity, and precision mechanics are converging to move humanoid robotics from factory floors into broader commercial and consumer environments faster than earlier robotics waves. For manufacturers, the value proposition is expanding beyond headcount substitution. Humanoid robots can support safer production environments, reduce downtime, improve inspection accuracy, stabilize labor-intensive workflows, and provide flexible automation in plants where traditional fixed robotics cannot easily adapt. This makes the category particularly relevant for automotive, electronics, logistics, aerospace, industrial equipment, healthcare support, and advanced manufacturing ecosystems. Segment Outlook: Fastest-Growing Opportunities Across the Humanoid Robots Market By Motion Type: Biped humanoid robots are expected to command the highest strategic attention, with MMR indicating a 2025 market share of about 61% and a stronger CAGR range than wheel-drive robots. Biped designs are favored because stairs, narrow aisles, hospital corridors, factories, and homes are built around human movement. By Offering: Hardware currently represents the largest share of robot value, supported by actuators, sensors, battery systems, embedded controllers, joints, motors, and end effectors. However, MMR identifies software as the future value migration layer, led by AI foundation models, motion-control operating systems, simulation platforms, digital twins, navigation software, and human-robot interaction systems. By Technology: Artificial intelligence, machine learning, deep learning, edge AI, computer vision, natural language processing, and real-time processing are becoming core technology categories for humanoid robots. These technologies support perception, autonomous navigation, environment mapping, manipulation, task learning, and decision-making. By Application: Personal assistance and caregiving, industrial and manufacturing, logistics, healthcare, retail and hospitality, education, entertainment, research, defense, security, and search-and-rescue are the key application areas identified in MMR's segmentation. Industrial and manufacturing applications are gaining relevance as factories accelerate flexible automation and smart production strategies. By Autonomy Level: Semi-autonomous and fully autonomous humanoid robots are expected to gain stronger enterprise interest as AI models mature, sensor fusion improves, and robot learning shifts from manual programming to simulation-based and imitation-based training. Recent Developments: AI Integration, Robotics Investments and Industrial Automation Platforms The competitive landscape is intensifying as robotics, semiconductors, AI software, automotive, and factory automation companies compete to control the 'brain,' 'body,' and deployment layer of humanoid robots. MMR identifies NVIDIA, Alphabet, Microsoft, Meta, and Baidu among key foundational AI and software ecosystem participants, with NVIDIA associated with Project GR00T, Omniverse, and Jetson; Alphabet linked to DeepMind robotics and Apptronik; Microsoft associated with Azure AI and Figure AI; and Baidu connected with robotics R&D and UBTech. In industrial infrastructure, Siemens is identified by MMR as a full automation-stack player with factory-wide humanoid integration and simulation capability, while Rockwell Automation is associated with factory integration of humanoid robots. These developments point to a future in which humanoids will not operate as standalone machines, but as nodes inside integrated smart manufacturing architectures combining digital twins, industrial simulation, robotics software, and process control systems. Component innovation is also accelerating. MMR lists Shenzhen Inovance's 2025 motor and actuator launch for humanoids, Will Semiconductor's 2024 2MP global shutter sensor launch for humanoids, Robosense's lidar and camera systems, Novanta's 6-axis force sensors, Keyence's machine vision and optical sensors, and Sony's image sensors for humanoid vision. These advancements are important because sensing density, actuator precision, edge processing, and motion-control reliability directly influence robot dexterity, safety, energy efficiency, and factory readiness. Country Trends: Mandatory Regional Insights United States: The U.S. is positioned by MMR as the AI brain, platform, and capital-markets hub of the humanoid robotics ecosystem. NVIDIA, Tesla, Alphabet, Microsoft, Amazon, Figure AI, Agility Robotics, and Boston Dynamics strengthen the country's role in AI software, compute, full-system integration, cloud robotics, and deployment funding. MMR also indicates the United States recorded 1,483 humanoid-related patents over five years, focused on higher-value AI and software patents. United Kingdom: The UK is included in MMR's Europe forecast scope. Its opportunity is aligned with Europe's broader role as a regulatory, industrial automation, AI governance, and advanced engineering market. Adoption is expected to be shaped by safety standards, labor-market policy, healthcare robotics needs, logistics modernization, and industrial digitalization. Germany: Germany is one of Europe's most important humanoid robotics opportunity centers because of its industrial automation base, automotive manufacturing depth, and precision-engineering ecosystem. MMR identifies Germany within Europe's key countries and lists German companies such as Siemens, Infineon, and Schaeffler across automation, motion control, power management, bearings, and linear guides. Japan: Japan remains a core precision robotics market. MMR highlights Japan's 30-year precision robotics manufacturing heritage and identifies companies such as Toyota, Sony, Nidec, Renesas, Harmonic Drive Systems, Nabtesco, NSK, THK, and Keyence across integrators, sensors, reducers, actuators, motors, machine vision, and robotics components. Japan's aging workforce and high automation intensity create a strong structural case for humanoid adoption. South Korea: South Korea is emerging as a strategic humanoid robotics hub through autos, memory chips, batteries, and consumer electronics. MMR notes that Samsung and Hyundai are driving Korean IP buildup, while Hyundai's ownership of Boston Dynamics gives South Korea a distinctive combination of automotive manufacturing scale and advanced locomotion IP. Samsung Electronics, SK Hynix, Hyundai, LG Energy, Rainbow Robotics, and LG Electronics are cited in the ecosystem. China: China is positioned as the dominant manufacturing and supply-chain force. MMR states that China filed 5,688 humanoid patents over five years, compared with 1,483 in the United States, and highlights that Asia-based companies account for 73% of the confirmed humanoid value chain. UBTech, Unitree, XPeng, BYD, GAC, Xiaomi, Robosense, CATL, EVE Energy, Sanhua, LeaderDrive, and other Chinese companies are advancing across robots, batteries, sensors, actuators, motors, thermal systems, and vision platforms. India: India is identified by MMR as an emerging demand market and software talent pool, supported by the National Robotics Mission 2023. While lower labor costs may slow near-term ROI compared with high-wage economies, India's long-term potential is linked to software development, deployment services, manufacturing modernization, logistics automation, and large-scale industrial digitization. Analyst Commentary 'According to Dharati Raut BE Research Analyst Automation & Process Control, Research Manager at Maximize Market Research, the humanoid robots market is moving into a strategic deployment phase where AI-driven automation, digital twins, predictive maintenance, IIoT connectivity, and energy-efficient manufacturing systems are becoming boardroom priorities. The next wave of growth will be shaped by companies that can combine reliable hardware, scalable software, industrial safety, lifecycle services, and regional deployment strategies. Humanoid robots are not merely an automation product; they are becoming a platform for industrial transformation.' Future Outlook: Energy-Efficient Automation and Next-Generation Process Control The next phase of the humanoid robots market will be defined by cost compression, software differentiation, and deployment scale. Energy-efficient battery systems, lightweight materials, high-efficiency motors, thermal management, advanced force sensors, edge AI processors, and simulation-based training will improve commercial readiness. At the same time, robot-as-a-service models, predictive maintenance contracts, factory integration services, and AI software subscriptions are expected to create recurring revenue opportunities. For industrial leaders, the opportunity is immediate but selective. The strongest returns are expected in environments with high labor cost, repetitive workflows, safety risks, production variability, and a need for flexible automation. Smart factories, automotive plants, electronics manufacturing, logistics hubs, healthcare facilities, and advanced industrial campuses are likely to lead adoption. As humanoid robots become embedded in smart manufacturing, their impact will extend beyond automation into workforce design, factory architecture, process control, data strategy, and regional competitiveness. Maximize Market Research provides strategic insights, competitive intelligence, regional opportunity analysis, and segment-level assessment to help enterprises, investors, and technology leaders identify where humanoid robotics will create the next wave of industrial value.

Source: openPR.com